When a Job Is Completed the Journal Entry Involves a

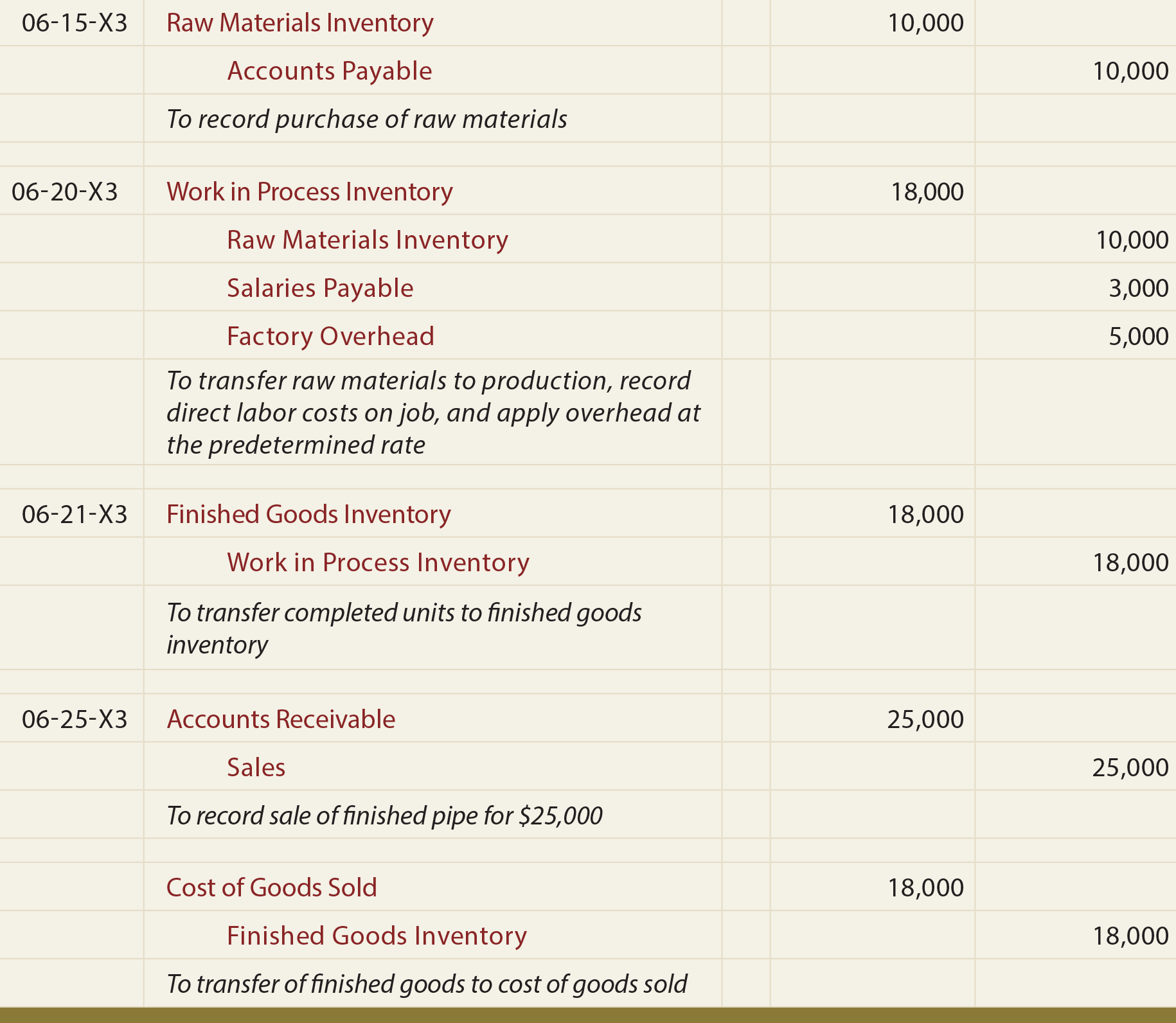

Journal entries are either recorded in subsidiary ledgers if youre keeping your. When each job and job order cost sheet have been completed an entry is made to transfer the total cost from the work in process inventory to the finished goods inventory.

Job Costing Material Labor Overhead Principlesofaccounting Com

C debit to cost of goods sold and a credit to finished goods inventory.

. In the second step of the accounting cycle your journal entries get put into the general ledger. And follows the matching and revenue recognition principles. The accounts into which the debits and credits are to be recorded.

This lesson will cover how to create journal entries from business transactions. The name of the person recording the entry. These entries are called journal entries since they are entries into journals.

Debit to Work in Process Inventory. Baines Company has the following estimated costs for next year. When a job is completed the total cost of manufacturing the job should be moved to which of the following general ledger accounts.

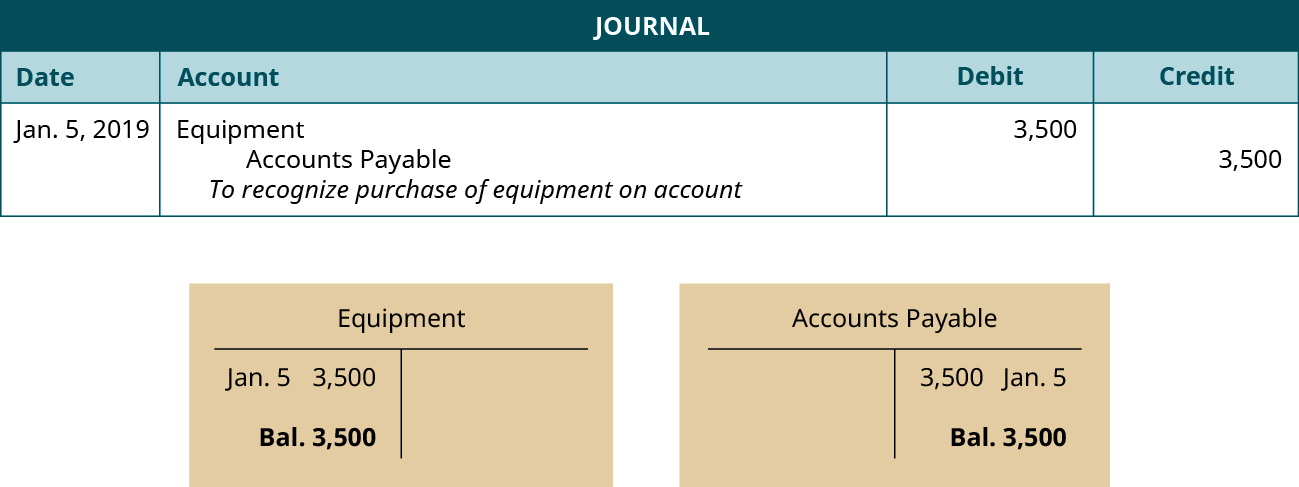

Generally adjusting journal entries are made for accruals and deferrals as well as estimates. Journal entries are how you record financial transactions. On December 7 the company acquired service equipment for 16000.

Two separate columns for debit and credit. This will result in a compound journal entry. To learn more launch our free accounting courses Free Courses.

1 Answer to 51 When a job is completed the journal entry involves a. Journal Entry to Move Work in Process Costs into Finished Goods. Direct materials 25000.

Every journal entry in the general ledger will include the date of the transaction amount affected. The journal entries follow the job costing process from purchase of raw materials allocation of direct materials direct labor and manufacturing overhead to work in process. AListing all accounts debited before any creditsBComputing the balances in accounts involved in the transaction.

B debit to finished goods inventory and a credit to work in process inventory. Debit to Finished Goods Inventory account and a credit to WorkinProcess Inventory account. An adjusting journal entry is usually made at the end of an accounting period to recognize an income or expense in the period that it is incurred.

Finished goods Ac Dr XXXXX To Work in process Ac XXXXX Being the job is completed When a job is completed we debited the finished goods account as the job is completed and credited the work in process account so that the proper posting could be done. CIndicating the date of transaction. There is an increase in an asset account debit Service Equipment 16000 a decrease in another asset credit Cash 8000 the amount paid and an increase.

A debit to work in process inventory and a credit to finished goods inventory. Journal Entry Examples. A a debit to finished goods inventory and a credit to work in process inventory for the cost of the job B a debit to finished goods inventory and a credit to.

The date of the journal entry. Example 1 Borrowing money journal entry. Format of the Journal Entry.

It is a result of accrual accounting. Have a go at writing journal entries for the transactions weve had in the previous lessons. Debit to Finished Goods Inventory account and a credit to Work-in-Process Inventory account.

Updated January 9 2021. At a minimum an accounting journal entry should contain the following components. Since most businesses use a double-entry accounting system every financial transaction impact at least two accounts while one account is debited another account is credited.

A journal entry is the first step in the accounting cycle. Debit to Cost of Goods Sold b. Here are numerous examples that illustrate some common journal entries.

This entry records the completion of Job 106 by moving the total cost FROM work in process inventory TO finished goods inventory. When a job is completed the journal entry involves a. The total job cost of Job 106 is 27950 for the total work done on the job including costs in beginning Work in Process Inventory on July 1 and costs added during July.

The company paid a 50 down payment and the balance will be paid after 60 days. Credit to Finished Goods Inventory. A reference number or also known as the journal entry number which is unique for every transaction.

The accounting period in which the journal entry should be recorded. The date of the entry. Journal entries are the way we capture the activity of our business.

The job cost accounting journal entries below act as a quick reference and set out the most commonly encountered situations when dealing with the double entry posting of job costing. Debit to Cost of Goods Sold and a credit to the Finished Goods Inventory account. Debit to Finished Goods Inventory.

Double-entry bookkeeping in accounting is a system of bookkeeping so named because every entry to an account requires a corresponding and opposite entry to a different account. When a job is completed in a job costing system the journal entry involves which accounts. To make a complete journal entry you need the following elements.

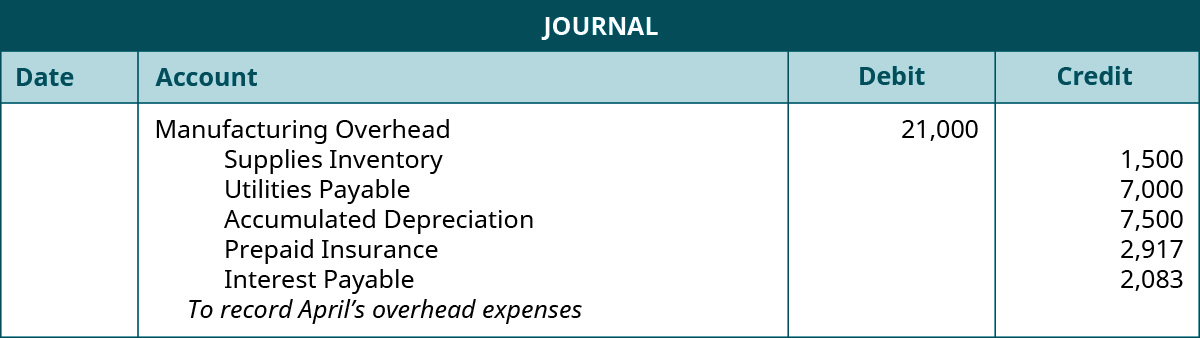

Hence our journal entry will involve a debit movement to expenses a credit movement to a bank just as we saw before. The journal entry to record the manufacturing overhead for Job MAC001 is. A journal details all financial transactions of a business and makes a note of the accounts that are affected.

The first example is a complete walkthrough of the process. The journal entry to record when a job is completed is shown below. Each journal entry includes the date the amount of the debit and credit the titles of the accounts being debited and credited with the title of the credited account being indented and also a short narration of why the journal entry is being recorded.

The best way to master journal entries is through practice. The journal entry to record when a job is completed would include a. When a job is completed the journal entry involves a.

Preparing a journal entry in proper form involves all the followingexcept. To make a journal entry you enter details of a transaction into your companys books. Journal entries are used to record the financial activity of your business.

The account column where you put the names of the accounts that have changed. DProviding a brief written explanation of the transaction. Now its your turn.

Prepare Journal Entries For A Job Order Cost System Principles Of Accounting Volume 2 Managerial Accounting

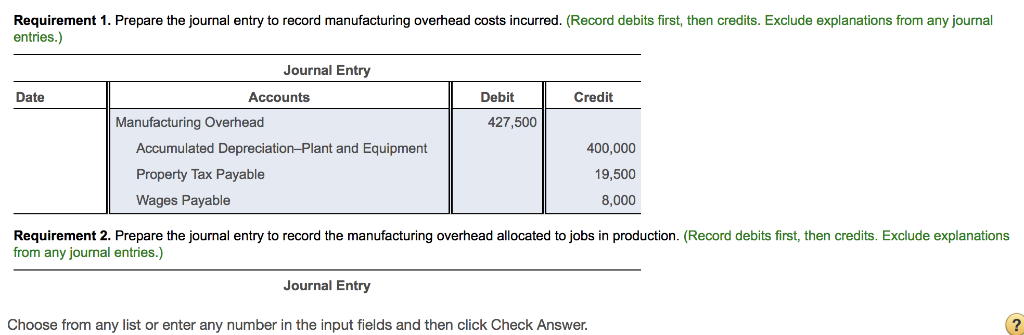

Solved Requirement 1 Prepare The Journal Entry To Record Chegg Com

Use Journal Entries To Record Transactions And Post To T Accounts Principles Of Accounting Volume 1 Financial Accounting

The Basic Accounting Journal Entries

No comments for "When a Job Is Completed the Journal Entry Involves a"

Post a Comment